LATEST NEWS

Insurance for Yachts: Everything Owners Need to Know

Insurance for yachts is one of the most relevant topics for anyone who invests in a high-end vessel, and also one of the most overlooked aspects at the time of purchase.

Protecting an asset of this magnitude requires more than a generic policy. It requires knowledge, planning, and the right choices.

Yacht owners face risks that go far beyond land-based concerns. Collisions, storms, and third-party liability are some of the situations that a well-structured policy must cover.

In this guide, you will find everything you need to know about how much insurance for a yacht costs, which types of protection exist, what influences the price, and how to choose the right option for your usage profile.

What Is Yacht Insurance and How Does It Work?

Yacht insurance is a specialized form of marine coverage designed to protect privately owned recreational vessels against financial losses resulting from accidents, theft, physical damage, liability claims, and other unforeseen events.

Unlike standard boat policies, it is tailored to larger, higher-value yachts that require broader protection and higher liability limits.

It works as a legal agreement between the owner and the insurer, defining the vessel’s insured value, selected protections, approved navigation area, exclusions, deductibles, and claim requirements.

If a covered event occurs during the policy period, the insurer pays for eligible losses according to the policy terms and limits.

Key Differences Between Yacht and Boat Insurance

Many owners use boat and yacht insurance as if they were the same thing, but the difference is more significant than it may seem.

Understanding where standard boat policies end and specialized insurance for yachts begins is essential when choosing the right protection.

See the comparison below:

| Criteria | Boat Insurance | Yacht Insurance |

| Typical size | Up to 26 feet | Above 26 feet |

| Insured value | Lower | High or very high |

| P&I coverage | Optional or limited | Essential and comprehensive |

| Crew coverage | Rarely included | Frequently required |

| Cruising area | Local or regional | National and international |

| Environmental coverage | Basic | Includes OPA and marine damage |

| Customization | Limited | High, tailored to the owner |

| Average annual cost | Lower | 1% to 3% of insured value |

The distinction is not merely technical. It reflects the level of operational complexity, the asset value involved and the legal responsibility that comes with owning a large vessel.

Read more: What makes a boat a yacht: size, structure, and build standards

What Does Insurance for Yachts Typically Cover?

A comprehensive insurance for yachts policy goes well beyond the physical protection of the vessel. Here are the core coverages to know:

- Hull & Machinery (H&M): protects against physical damage from collisions, fires, storms and groundings, covering engines, electrical systems and onboard equipment.

- Protection & Indemnity (P&I): addresses civil liability for damage caused to third parties, other vessels and properties, as well as injury claims from passengers and crew.

- Agreed Value vs. Actual Cash Value: with Agreed Value, the fixed amount is paid in full upon total loss, with no depreciation deducted. Actual Cash Value factors in depreciation, which typically results in a lower settlement.

Factors That Influence Yacht Insurance Cost

Understanding how much does yacht insurance cost starts with knowing what underwriters evaluate. Annual H&M premiums typically range from 1% to 3% of the insured value.

A yacht valued at €5 million, for instance, may generate between €50,000 and €150,000 per year.

Six factors drive the final premium:

- Size and value of the vessel, reviewed annually to avoid misvaluation

- Age and condition, with wooden hulls attracting higher rates than GRP

- Cruising area, as worldwide coverage costs more than regional policies

- Claims history, where a clean record over 3 to 5 years unlocks discounts up to 30%

- Vessel use, with commercial charter operations carrying higher premiums than private use

- Safety equipment, including AIS transponders, EPIRBs and fire suppression systems

How Yacht Insurance Claims Work

Filing a claim under an insurance for yachts policy follows a clear sequence. Knowing each step in advance helps prevent mistakes that could compromise the settlement.

The process works as follows:

- Report the incident promptly: most policies require notification within 24 hours of a serious event, along with supporting documentation.

- Damage assessment: the insurer appoints a surveyor to evaluate the damage and determine repair costs.

- Claim settlement: partial losses are paid based on repair costs. In a total loss, Agreed Value pays the contracted amount, while ACV deducts depreciation.

What to Evaluate Before Choosing a Policy

Before signing any policy, four points deserve close attention:

- Valuation basis: Agreed Value offers greater predictability for high-value yachts, while ACV deducts depreciation at the time of loss.

- Cruising area: confirm the policy covers every region you plan to navigate. Sailing outside the defined area may void coverage entirely.

- Exclusions: read carefully what is not covered. Wear and tear, osmosis, electrolysis, war, piracy and marine life damage are common exclusions.

- Deductibles: a higher deductible lowers the premium but increases out-of-pocket exposure. Finding the right balance is especially important for owners looking to preserve a no-claims discount.

When comparing insurers, look beyond the premium. Consider financial strength, claims payment history, surveyor network, and emergency support quality.

Working with an experienced marine broker is highly recommended, as they understand the niche market, have relationships with underwriters, and can negotiate terms tailored to your yacht’s use.

Common Mistakes When Buying Insurance for Yachts

Even experienced owners make avoidable mistakes when managing yacht insurance. The most common ones are:

- Ignoring the cruising area: sailing beyond the policy’s defined limits without notifying the insurer can void coverage entirely in the event of an incident.

- Failing to declare charter use: private-use policies do not cover commercial operations. If the yacht is used for charter, the policy must reflect that.

- Choosing by price alone: the lowest premium rarely means the best protection. Evaluating coverages, exclusions and the insurer’s reputation matters as much as the cost.

Read more: Yachting tips for beginners: tips for starting with safety and confidence

A Reliable Yacht Is Your First Line of Protection

Before choosing insurance, the first priority is selecting a yacht you can rely on. A well-built model reduces risk from the very beginning — and that is where NX Boats stands apart.

From 26 to 62 feet, every NX model combines technical precision, contemporary design and refined finishes that make a real difference on the water.

With over 550 qualified professionals, a proprietary 20,000 m² facility and operations in markets such as Brazil, the United States, Turkey and Switzerland, NX Boats offers not only premium yachts, but also continuous support, structured after-sales service and a lasting relationship with every owner.

Discover the NX Boats lineup and see the difference for yourself.

FAQ

What Is the 10% Rule for Yachts?

The 10% rule suggests that the annual premium should not exceed 10% of the yacht’s insured value. In practice, H&M premiums usually range from 1% to 3%.

What Are the Three Types of Marine Insurance?

The main types are Hull & Machinery (H&M), Protection & Indemnity (P&I), and Cargo Insurance. For private yachts, H&M and P&I are the most relevant.

What Are the Four Types of Insurance for Yachts?

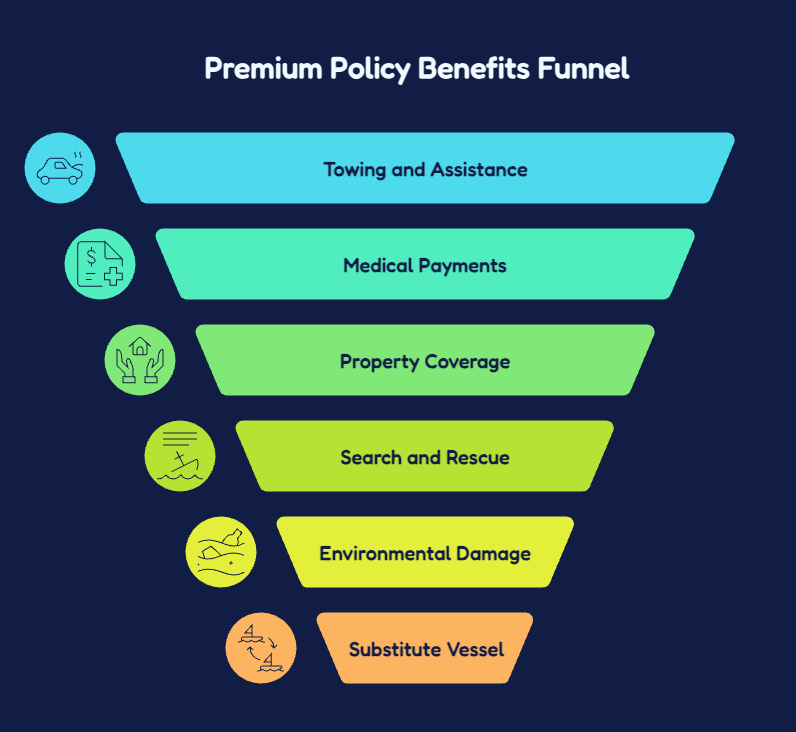

Standard yacht coverage often includes Hull & Machinery, Protection & Indemnity, Medical Payments, and Personal Property.

Um novo mundo está surgindo, e a NX Boats faz parte dessa mudança, estamos revolucionando o design, unindo conforto e modernidade tudo isso por que queremos proporcionar a melhor experiência para quem navega com uma NX.